…Easing inflation and resilient global commerce offer some reasons for optimism but fiscal challenges loom large.

…53% of chief economists identify public debt as a major risk to stability in advanced economies; 64% express similar concerns for developing economies.

…Almost 40% of experts surveyed expect defaults to rise in developing economies over the next year.

WED SEPT 25 2024-theGBJournal|Easing inflation and strong global commerce are fuelling cautious optimism for recovery but elevated debt levels are becoming a growing concern in both advanced (53%) and developing (64%) economies, according to the latest Chief Economists Outlook published today by the World Economic Forum.

The report, based on a survey of leading chief economists, highlights that debt levels and fiscal challenges are placing significant pressure on economies worldwide leaving them vulnerable to future crises. A growing concern is a potential “fiscal squeeze”, where rising debt-servicing costs limit governments to invest in essential sectors such as infrastructure, education and healthcare. In developing economies, 39% of economists expect an increase in defaults over the next year.

“The global economy may be stabilizing, but fiscal challenges continue to pose significant risks,” said Saadia Zahidi, Managing Director, World Economic Forum. “Addressing these challenges requires coordinated efforts from policy-makers and stakeholders to ensure that economic recovery is not undermined by these pressures. Now is the time for pragmatic solutions that can strengthen both fiscal resilience and long-term growth.”

Regional outlook: Diverging economic growth and debt risks

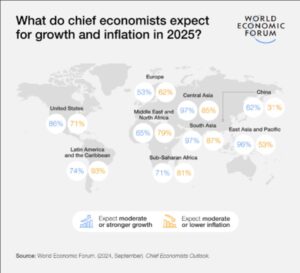

The global economic outlook varies sharply across regions. In the United States, nearly 90% of chief economists anticipate moderate or strong growth in 2024 and 2025 reflecting confidence in a “soft landing” after a period of tight monetary policy. Some 80% of those surveyed agree that the outcome of the United States election will significantly influence global economic policy, with many citing election-related risks as a major concern for the year ahead.

In contrast, nearly three-quarters of respondents expect weak growth for the remainder of the year in Europe. Similarly, China’s struggles persist, with almost 40% of economists forecasting weak or very weak growth in both 2024 and 2025.

Elsewhere, growth prospects are mixed. In sub-Saharan Africa, a moderate or stronger growth trajectory is anticipated, with expectations improving from 55% in 2024 to 71% in 2025. The Middle East and North Africa region remains uncertain, while Latin America is expected to see modest improvements, with a slight uptick in growth in 2025. South Asia also stands out, with over 70% of economists predicting strong or very strong growth in 2024 and 2025, driven by India’s robust performance.

Global inflation continues to ease, with many chief economists expressing optimism for next year. In the US, the share of chief economists expecting high inflation drops from 21% in 2024 to 6% in 2025. Europe is expected to follow a similar trend, with high expectations for high inflation dropping from 21% this year to 3% next year, providing some relief to policy-makers.

While a majority of chief economists (54%) expect the condition of the global economy to remain stable in the short term, 37% foresee conditions will weaken, compared to only 9% who expect an improvement.

Challenges in achieving better balanced growth

Policy-makers are facing growing pressure to balance economic growth with other priorities, such as environmental sustainability, economic equality, and social cohesion. Two-thirds of respondents agree that progress on these goals is necessary, even if it slows growth. However, only 12% believe current efforts are effective.

Political polarization (91%) and the lack of global cooperation (67%) are identified as major barriers to achieving progress on more balanced growth. But with rising geopolitical tensions and domestic political divisions, prospects for improvement in the short term appear bleak.

Greater political consensus and international collaboration will be essential to balance the quality and quantity of growth, as per the new report.

Long-term economic risks

Looking ahead, the report highlights that limited fiscal space leaves countries ill-prepared for future crises, particularly in developing economies (82%) compared to advanced economies (59%).

The growing burden of debt is not only a short-term threat to macroeconomic stability but also hampers the ability of countries to address long-term challenges such as climate change, demographic shifts and social cohesion. If debt sustainability remains a significant constraint on countries’ ability to spend, economies may struggle to maintain sustainable growth while navigating these pressing global issues.

X-@theGBJournal|Facebook-the Government and Business Journal|email:gbj@govbusinessjournal.com|govandbusinessj@gmail.com

{kind=link}