…This economic note unpacks the Q4 2025 debt data across four analytical lenses: composition and trajectory, fiscal sustainability, subnational dynamics, and forward implications for macroeconomic policy and investor positioning.

WED MAY 06 2026-theGBJournal| Nigeria’s National Bureau of Statistics (NBS) released the Nigerian Domestic and Foreign Debt Report for Q4 2025, revealing a total public debt stock of N159.28 trillion ($110.97 bn), a 3.90% increase from N153.29 trillion in Q3 2025, and N14.6 trillion above the N144.67 trillion recorded in Q4 2024.

On the surface, the numbers appear relatively reassuring, though may not fully reflect the underlying reality.

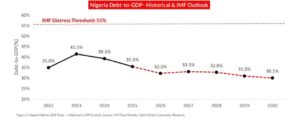

Nigeria’s debt-to-GDP ratio which stood at 39.3% in 2024, remains well below the IMF’s 55% distress threshold, and the IMF’s April 2026 Fiscal Monitor projects a further decline to 32.3% by 2026. Yet the headline ratio tells an incomplete story.

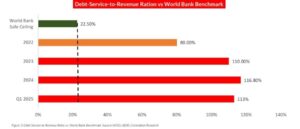

The more structurally revealing metric; the debt-service-to-revenue ratio, remains critically elevated at an estimated 113% in Q1 2025 as reported in Macroeconomic Condition Index report by Nigerian Economic Summit Group (NESG), indicating that debt obligations continue to exceed all federal revenue earned in a given period.

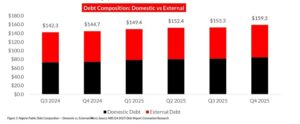

Domestic Debt Vs External Debt

At the end of Q4 2025, domestic debt of N84.85 trillion constituted 53.37% of total public debt, while external obligations of N74.43 trillion accounted for the remaining 46.73%.

This split reflects the Federal Government’s deliberate tilt toward external financing as domestic borrowing costs remain elevated in the wake of the CBN’s hawkish monetary stance.

Domestic debt is predominantly composed of FGN Bonds, Treasury Bills, and CBN Promissory Notes. The high stock of rollover intensive instruments amplifies refinancing risk.

On the external side, the portfolio blends multilateral concessional loans (World Bank IDA, AfDB, IMF), bilateral obligations (China EXIM, France AFD), and commercial instruments including Eurobonds, which as of 2024 stood at about $18.55 billion — roughly 35.77% of total external debt

Debt Accumulation Trend

Nigeria’s public debt stock has more than tripled since Q1 2023, rising from N49.85 trillion to N159.28 trillion by Q4 2025, a N109 trillion expansion in under three years. The drivers have shifted across the period.

In 2023–2024, the CBN’s naira’s unification policy which collapsed the official rate from N899/$ to N1,535/$ was the dominant force, mechanically inflating the naira value of external obligations.

In 2025, the dynamic reversed as naira appreciated into the N1,400s in Q3 2025, Despite this FX tailwind, the N14.6 trillion year-on-year increment reflects pure structural borrowing pressure — external debt alone grew by $6.07 billon in dollar terms ($45.78bn to $51.80 billion), underpinned by a $2.35 billion dual-tranche Eurobond issuance in November 2025 and

continued multilateral and bilateral drawdowns.

The growth despite the Naira appreciation is perhaps the more telling signal.

The National Assembly’s March 2026 approval of a $6 billion external borrowing package — a $5 billion TRS facility with First Abu Dhabi Bank and a $1 billion UK Export Finance-backed port facility — confirms the trajectory would likely continues into 2026.

The Debt-to-GDP Optic — Reassuring but Incomplete

Nigeria’s debt-to-GDP ratio of approximately 32–35% is frequently cited by government spokespersons and IMF projections to argue that Nigeria’s debt load is manageable by international standards.

The IMF’s April 2026 Fiscal Monitor projects Nigeria’s ratio declining from 35.5% in 2025 to 32.3% in 2026, before settling at approximately 33.1% in 2027 and 30.1% by 2031.

These projections incorporate the positive effect of the NBS GDP rebasing exercise, which meaningfully enlarged the denominator.

However, the GDP ratio is not the primary stress variable for Nigeria’s fiscal condition. The country’s revenue base, not the size of its economy, is the binding constraint on debt sustainability, and it is structurally undersized relative to African peers.

At about 9–10% of GDP, Nigeria’s tax-to-GDP ratio sits far below South Africa (24%), Kenya (16%), and Ghana (13%), and below the Sub-Saharan Africa average of 15%.

Debt-Service-to-Revenue: The Critical Gauge

The NESG estimates Nigeria’s debt-service-to-revenue ratio at approximately 113% in Q1 2025, structurally far above the World Bank’s recommended ceiling of 22.5%.

In January 2025 alone, the CBN’s Monthly Economic Report captured debt service obligations of N696.27 billion against total retained revenue of only N483.47 billion — a single-month coverage ratio of approximately 144%.

The Budget Office’s MTEF/FSP data for January–July 2025 showed federal revenue of N13.67 trillion against a prorated target of N23.85 trillion, a N10.19 trillion (42.7%) shortfall.

Oil revenue was the key driver of this shortfall at 62.2% below plan. Non-oil gains in CIT and VAT were insufficient to compensate.

The implication is that a government spending more on debt servicing than it earns in total revenue is not servicing debt from cash flow — it is rolling obligations forward, creating a self-reinforcing borrowing cycle.

Subnational Debt Dynamics

The NBS Q4 2025 report provides subnational granularity that is analytically important for a better understanding of the distribution of fiscal risk across the Federation.

Domestic Debt Concentration

Lagos State recorded the highest domestic debt stock at N1.22 trillion in Q4 2025, followed by Rivers State at N378.81 billion.

At the other end, Jigawa State carries the lowest domestic debt at N1.60 bn, followed by Ondo at N8.42 billion.

The concentration in Lagos and Rivers is not surprising given their economic primacy, but it also means states with large domestic debt portfolios will face rising debt service pressure as interest rates remain elevated, crowding out capital expenditure.

External Debt: Concentration and Concessional Access

Lagos State dominates subnational external debt as well, at $1.17 billion, followed by Kaduna State at $684.29 million.

FCT records the lowest external exposure at $26.80 million, followed by Zamfara at $41.93 million. Subnational external debt is predominantly project linked, backed by World Bank, AfDB, and bilateral lenders, and is structurally more resilient than commercial borrowing, benefiting from concessional rates and tied disbursements.

Crucially, only approximately 8% of total public debt stock is owed by state governments, making debt sustainability fundamentally a federal government issue — a key distinction for investors and rating agencies.

Revenue Mobilisation as the Decisive Variable

The IMF’s Article IV (2025) and Fiscal Monitor (April 2026) consistently identify revenue mobilization, not simply borrowing restraint, as the central policy imperative.

Nigeria’s tax-to-GDP ratio of approximately 9–10% sits below the Sub-Saharan Africa average of 15%, and every percentage point gain materially alters the fiscal trajectory.

Non-oil revenue through FIRS reform, VAT broadening, and improved compliance remains the most credible path to a sustainable debt service/revenue ratio.

Exchange Rate and External Debt Valuation

Because 46.73% of Nigeria’s debt is denominated in or valued in foreign currency, Naira volatility directly affects the reported Naira value of the external debt stock.

A weaker naira inflates the NGN-equivalent of external obligations as reported by the DMO, without any new borrowing, as seen most sharply in 2023–2024 when the naira’s collapse from N899/$ to N1,535/$ drove a mechanical expansion in the headline debt stock.

The 2025 appreciation reversed this, compressing the naira-equivalent of the debt stock (total debt grew 10.10% in naira terms versus 17.78% in dollar terms, with the naira appreciation absorbing the difference) and contributing to the improvement in the debt-to-GDP ratio from 39.3% to 35.5%.

The IMF projections to 2031 are therefore sensitive to exchange rate assumptions — any sustained depreciation would push the ratio back up independent of fiscal behaviour.

Appetite for New External Borrowing

The FG’s $6 billion (including $5 billion Total Return Swap facility with First Abu Dhabi Bank and a $1 billion UK Export Finance) additional external borrowing approval in March 2026 signals continued reliance on debt markets for deficit financing.

The stated preference for bilateral (UAE, UK) is policy-positive to the extent it secures lower-cost, longer-tenor financing, compared to commercial issuance. Separately, Nigeria’s Eurobond spreads have rallied on the back of reform momentum and oil price optimism —a sign of restored commercial market access.

However, this is susceptible policy reversal, or a global risk-off episode, any of which could raise the cost of future commercial issuance significantly. A pre-election fiscal spending uptick in 2026–2027 is an additional risk variable to monitor.

Structural Reform Imperatives

-Fiscal Responsibility Act Enforcement: The Fiscal Responsibility Commission should be empowered with investigative authority and clear penalties for violations.

Borrowing for recurrent expenditure rather than capital investment contravenes the Act.

-Debt Sustainability Analysis Restoration: The DMO’s DSA reports, a routine publication since 2008, appears to have been discontinued. Reinstatement would materially improve debt transparency and investor confidence.

-Revenue Diversification: Beyond NRS reform, CGT, stamp duties, property taxation, and mining/solid minerals royalties offer significant upside that remains chronically underexploited.

-Contingent Liability Management: State-level debt arrears, SOE liabilities, and off-budget financing arrangements constitute a shadow balance sheet that formal debt statistics understate.

Conclusion

Nigeria’s Q4 2025 public debt stock of N159.28 trillion ($110.97 billion) is a number that requires contextual reading to fully understand what it means. The headline figure and debt-to-GDP metrics present a fairly healthy picture by emerging market standards; the IMF’s 32.3% projection for 2026 offers genuine comfort.

But the debt-service-to-revenue ratio — running at an estimated 113% in early 2025 — tells a different story: one of a government under acute cash flow stress, financing current obligations through incremental borrowing.

The Q-o-Q acceleration of 3.90% in Q4 2025 is not alarming in isolation. But set against a backdrop of persistent revenue underperformance, rising interest costs, and a possible $6 billion of new borrowings, it reinforces our view that Nigeria’s fiscal consolidation story is in reality still aspirational as it is fragile in execution.

Revenue mobilisation — not debt management descriptive — is the variable that will determine whether the sustainability trajectory genuinely improves.

…This ECONOMIC NOTE is written by analysts at Coronation Research

X-@theGBJournal|Facebook-the Government and Business Journal|email:gbj@govbusinessjournal.com|govandbusinessj@gmail.com

https//www.govbusinessjournal.com<Business>External Debt

{kind=link}