…Government expenditure is expected to remain elevated, even as potential revenue improvements provide some fiscal reinforcement.

…Debt service costs (NGN16.44 trillion vs 2025E: 15.82 trillion | Budget: NGN15.81 trillion) are also expected to remain high, primarily due to elevated interest rates and a rising total debt stock.

By Esther Mayowa

THUR APRIL 30 2026-theGBJournal| The 2026 Federal Government budget was signed into law by the President on 17 April, following its approval by the National Assembly on 31 March.

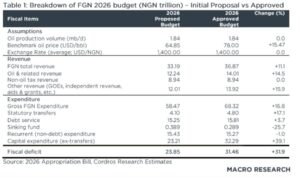

The approved budget reflects a 16.8% increase to NGN68.32 trillion from the initial NGN58.47 trillion proposal.

The revision primarily reflects a more optimistic revenue target as well as higher capital spending. Despite these revisions, we expect budget underexecution to persist, largely driven by continued shortfalls in capital spending.

Elsewhere, recent reforms in the oil and tax sectors are poised to strengthen revenue mobilisation, supporting a notable improvement in overall revenue performance, albeit still below the government’s projections.

Accordingly, we anticipate the fiscal deficit to come in below the official target. Nonetheless, our estimates suggest financing needs are expected to remain elevated, with borrowings continuously skewed towards the domestic market, likely keeping yields higher in the near term.

About three months into the fiscal year without an enacted budget, the National Assembly approved the 2026 Federal Government budget, which was subsequently signed into law by the President on 17 April. The approved budget of NGN68.32 trillion is a 16.8% increase from the NGN58.47 trillion earlier presented.

The upward revision primarily reflects a significant increase in capital expenditure allocations, alongside a modest adjustment to non-debt recurrent spending and a downward revision to debt service costs.

On the revenue side, projections were revised higher, largely reflecting increased oil revenue assumptions following an upward adjustment to the oil price benchmark, as well as stronger expected contributions from government-owned enterprises.

Notwithstanding the upward revision of the budget, we believe the credibility of the actual numbers will ultimately depend on how effectively revenues are realised and how well expenditure is executed.

Against this backdrop, we adopt a more cautious baseline than the government’s projections—acknowledging the positive momentum from ongoing reforms in the oil and tax sectors as well as elevated global crude prices, while remaining mindful of the structural and implementation constraints that have historically weighed on budget performance.

Reforms and Elevated Oil Prices May Strengthen Revenue Performance

We expect government revenue to improve from the previous year. This will be driven by the (1) combined impact of higher crude oil production and global prices, (2) reforms to the oil revenue remittance framework, and (3) tax reform implementation.

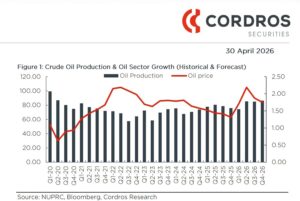

First, we maintain our expectations of stronger oil production (2026E: 1.73 mb/d vs 2025FY: 1.64 mb/d), driven by recent infrastructure upgrades—particularly the launch of Cawthorne crude via the FSO Cawthorne. This is expected to ease evacuation constraints and improve efficiency in OML 18 and surrounding assets.

According to Kpler (a global commodity data and analytics firm), the deployment of the FSO Cawthorne and the associated evacuation infrastructure is estimated to lift Nigeria’s crude production by approximately 50,000 bpd in 2026.

Beyond infrastructure, sustained investment by indigenous operators is expected to further strengthen output. Key players such as Seplat Energy Plc and Renaissance Africa Energy Company are accelerating brownfield redevelopment and drilling programmes to unlock previously shut-in volumes and improve recovery rates.

Seplat, for instance, has guided toward an average gross production of 135,000–155,000boepd in 2026 (vs. 131,506boepd in 2025FY), supported by an active drilling campaign (17 new wells to be drilled in 2026) and improved asset reliability.

Similarly, Renaissance is expected to sustain a material ramp-up in output, targeting production of around 300,000bpd by early 2026, driven by the reactivation of idle wells and expanded field development. In addition, ongoing efforts to curb crude theft and enhance pipeline surveillance are likely to reduce losses and support higher realised production volumes.

Crucially, higher production and improved operational efficiency are expected to translate into stronger government oil revenues. As output increases, royalty payments and profit oil are expected to rise, while improved metering and reduced leakages should ensure that more of this production is captured and taxed. At the same time, elevated global oil prices—supported by ongoing Middle East tensions and supply disruptions (Cordros estimate: USD90.00/bbl vs 2025FY: USD69.00/bbl)—are expected to further boost earnings by increasing the value of each barrel produced.

Most importantly, we note that recent reforms to oil-related deductions and remittance frameworks are expected to enhance net oil revenue accruals.

This includes (1) full remittance of Production Sharing Contract (PSC) profits to the Federation Account (only 40.0% was previously remitted, while 60.0% was retained for management fees & frontier exploration fund) by the Nigerian National Petroleum Company Limited (NNPC Ltd), (2) direct remittance of royalty and tax oil under PSCs, and (3) the redirection of gas flare penalties from the Midstream and Downstream Gas Infrastructure Fund (MDGIF) to the Federation Account.

Specifically, based on historical trends, we estimate that the PSC reform and the remittance of gas flare penalties to the federation account could potentially add c. NGN1.50 trillion to the federation account and c. NGN700.00 billion to the federal government revenue in 2026E, with higher oil prices likely providing upside.

Indeed, the NNPCL stated in its February monthly report that statutory remittances to the federation account soared by 147.9% to NGN1.80 trillion in February from NGN726.00 billion in January. The increase primarily reflects improved revenue capture following the implementation of the new remittance framework and reduced deductions at source.

Altogether, we project oil revenue to rise to NGN13.59 trillion, from NGN8.00 trillion in 2025E. That said, our estimate is slightly below the government’s projection of NGN14.01 trillion, primarily reflecting the risk of oil production underperforming the official benchmark of 1.84 mb/d.

This is due to persistent structural constraints, including ageing assets and recurring maintenance shutdowns, which continue to limit output expansion.

Furthermore, while recent investments are expected to support production over time, we believe their impact will materialise more meaningfully in the medium term than in the near term, as implied by the government’s projections.

Regarding tax revenue, the implementation of the 2025 tax reforms has commenced, with the core provisions of the Nigeria Tax Act and Nigeria Tax Administration Act taking effect from 1 January 2026.

We retain our view that key measures, such as (1) the digitalisation of tax administration, (2) enhanced tax compliance, and (3) stricter enforcement across key sectors, are likely to support stronger non-oil revenue mobilisation.

In addition, ongoing efforts to harmonise tax processes and reduce leakages across revenue-collecting agencies are expected to further boost collections.

Nonetheless, we believe the currency stability is likely to weigh on FX-linked tax revenues, thereby limiting the pace at which tax revenues exceed the government’s projection. We estimate tax revenue to reach NGN9.30 trillion, surpassing NGN7.50 trillion in 2025E and the government’s target of NGN8.94 trillion.

While we anticipate relative improvements in major other revenue components, such as GOEs (2026E: NGN2.58 trillion vs 2025E: NGN2.23 trillion | Budget: NGN5.85 trillion) and independent revenue (2026E: NGN3.66 trillion vs 2025E: NGN3.10 trillion | Budget: NGN4.31 trillion), performance is likely to remain subpar to fiscal targets primarily due to continued weak compliance and collection inefficiencies.

Overall, we project total revenue of NGN31.88 trillion (equivalent to 5.8% of GDP), which underperforms the government’s target of NGN36.87 trillion but reflects a strong improvement from 2025E (NGN23.43 trillion).

Ambitious Budget Expenditure May Face Execution Constraints

Government expenditure is expected to remain elevated, even as potential revenue improvements provide some fiscal reinforcement. However, we view the NGN68.32 trillion spending target as overly ambitious, given that recent revenue gains remain limited and insufficient to sustainably support such a high level of expenditure.

Specifically, we expect high personnel and overhead costs, as well as special intervention programmes, to keep non-debt recurrent spending (NGN13.04 trillion vs 2025E: NGN8.84 trillion) elevated, though still below budget (NGN15.43 trillion), likely due to under-execution of discretionary allocations.

Debt service costs (NGN16.44 trillion vs 2025E: 15.82 trillion | Budget: NGN15.81 trillion) are also expected to remain high, primarily due to elevated interest rates and a rising total debt stock.

Nonetheless, exchange rate appreciation may partially moderate external debt servicing costs in naira terms, thereby providing some relief to overall debt service pressures.

On capital spending, outturns are expected to fall well short of the budgeted NGN30.24 trillion (excluding project-tied loans of NGN2.05 trillion). We expect the underperformance to primarily stem from real-time financing constraints, administrative bottlenecks (including procurement delays and inefficient fund releases), ambitious targets, and weaknesses in the budget preparation process.

Notably, the preparation cycle is often characterised by late submission of the Appropriation Bill, prolonged legislative scrutiny, unrealistic project costing by Ministries, Departments and Agencies (MDAs), and weak alignment with actual cash availability and prior year execution performance.

This, in turn, has compounded implementation challenges and contributed to the continued extension of budget implementation timelines into subsequent fiscal periods (budget rollover cycles), thereby weakening the credibility of the budget as a reliable fiscal anchor.

Indeed, the 2024 capital budget achieved only about 84.0% execution, even after its implementation period was extended into 2025.

Similarly, preliminary data for 2025 indicate that only 17.0% of the capital allocation had been released by Q3-25, with approximately 70.0% of projects rolled over into 2026. Of this rollover, about 70.0% has been incorporated into the 2026 capital budget, while the remaining 30.0% is expected to run concurrently with the 2026 budget through November 2026, further exacerbating execution risks.

Given these challenges, we expect 2026 capital spending to achieve c. 60.0% execution, resulting in an outturn of roughly NGN18.00 trillion, well below the budgeted amount (NGN30.24 trillion).

Despite the anticipated underperformance, this represents a modest improvement relative to 2025 levels, supported by increased efforts to accelerate project delivery ahead of the 2027 elections and the partial consolidation of the 2025 capital budget rollover into the 2026 fiscal framework.

Combining our projections for recurrent and capital expenditure, we project total expenditure of NGN54.31 trillion (10.7% of GDP), including project-tied loans (NGN2.05 trillion) and statutory transfer (NGN4.80 trillion).

Given our revenue estimate of NGN31.88 trillion, the fiscal deficit is projected at NGN22.43 trillion (equivalent to 4.31% of GDP), surpassing an estimated NGN16.82 trillion in 2025E but undershooting the government’s estimate of NGN31.46 trillion.

Widening Deficit to Set the Stage for Heavier Borrowings

Although our fiscal deficit estimate remains materially below the government’s budget target, it still points to a sizeable financing requirement. Excluding project-tied loans (NGN2.05 trillion) and privatisation proceeds (NGN189.16 billion), we estimate total borrowings (comprising both domestic and external sources) at approximately NGN20.19 trillion (30.9% lower than the budget projection of NGN29.22 trillion).

Within this, domestic borrowing is expected to account for the dominant share, at NGN16.61 trillion, underscoring the government’s continued reliance on the local debt market to fund its obligations. This implies a sustained increase in sovereign issuance, which is likely to keep yields elevated in the short to medium term and heighten the risk of crowding out private-sector credit.

On the external side, foreign borrowing is projected at NGN3.58 trillion, broadly in line with the budget. As earlier highlighted in our note (Nigeria Embraces a New Frontier in External Borrowing), amid persistent global uncertainty, tight financial conditions, and elevated external borrowing costs, the government’s proposed USD5.00 billion Total Return Swap (TRS) facility with First Abu Dhabi Bank (FAB) may serve as a substitute for conventional Eurobond issuance in the 2026 budget.

Based on its external financing requirements, we expect the government to adopt a phased drawdown strategy, with an initial tranche of approximately USD2.00–2.50 billion likely in the second half of the year, when funding needs intensify.

Nonetheless, we do not rule out a reversion to Eurobond issuance should global uncertainty moderate and financial conditions ease, particularly considering the contingent risks, mark-to-market sensitivities, and potential margin call exposures inherent in the TRS structure.

The government may also complement its external financing mix with alternative sources such as syndicated loans from international and regional banks, bilateral and multilateral concessional funding (e.g., World Bank, AfDB), as well as export credit facilities tied to infrastructure and capital projects.

Despite the International Monetary Fund’s (IMF) recently expanded USD50.00 billion lending capacity aimed at supporting vulnerable economies facing external shocks, the Federal Government has indicated that it has no plans to access this facility. We believe this is likely due to the government’s preference to avoid the stringent fiscal consolidation requirements and policy conditionalities typically associated with IMF programmes.

Total Debt to Climb but Remain Sustainable

Based on our estimated borrowings (domestic & external) for 2026E and our year-end naira estimate of NGN1,350.00/USD, we project total debt to reach NGN179.27 trillion by year-end, reflecting a 12.6% increase from NGN159.28 trillion in 2025FY. Despite the increase, Nigeria’s debt remains within sustainable limits at 35.3% of GDP, well below the prudential thresholds of 55.0% and 60.0% set by the IMF and the Debt Management Office (DMO), respectively.

Risks to Our Estimate

We highlight key risks that could skew our fiscal deficit projection either higher or lower and, by extension, alter the government’s borrowing requirements in the debt market.

In a best-case scenario (upside risks), stronger-than-expected oil prices and more robust gains from ongoing revenue reforms could lift revenues above our baseline. At the same time, weaker-than-anticipated execution of capital projects—stemming from a shorter implementation period—could keep total expenditure below our estimate. Taken together, these dynamics would result in a narrower fiscal deficit than projected.

Conversely, the worst-case scenario (downside risk) assumes oil production falls short of our estimate, alongside a pullback in oil prices. In addition, reform-driven revenue gains could underperform due to implementation challenges, weakening overall revenue mobilisation. If expenditure remains elevated under this scenario, the fiscal deficit is expected to widen beyond our baseline projection.

Mayowa is analyst at Cordros Securities

X-@theGBJournal|Facebook-the Government and Business Journal|email:gbj@govbusinessjournal.com|govandbusinessj@gmail.com

{kind=link}