By Rebecca Jane Ellis

TUE APRIL 14 2026-theGBJournal| The global economic landscape has shifted into a phase of “economic aftershocks”. Structural damage to global energy infrastructure—specifically the Ras Laffan complex—has pushed Brent Crude past $100/bbl, making high energy costs a structural reality rather than a temporary spike.

For business owners and trustees, the “Inflationary Creep” of 2026 presents a direct threat: US inflation is holding between 3.4% and 4%. With US Federal Debt at 101% of GDP, the government has limited room to raise interest rates significantly without risking a sovereign debt crisis.

In this environment, a $100 million reserve in standard cash accounts can lose $4 million in purchasing power annually.

To preserve capital and enhance yields, we are pleased to present two institutional structures designed for the 2026 macro environment.

Strategic Option 1: USD Callable Daily Range Accrual Capital Preservation with Premium Yield Potential

This structure pays a daily rate for as long as the 10Y USD CMT Rate stays within a specific “high-neutral” band. This is ideal for an environment where high debt prevents rates from rising much further, while high inflation prevents them from falling.

-Capital Protection: 100% at maturity.

-Quarterly Coupons: The coupon is calculated based on a daily rate and is paid out quarterly.

-Issuer Callability: The issuer may call the note quarterly, starting after Year 1.

-Minimum Investment: $100,000 USD.

Strategic Option 2: Hybrid Credit-Linked Range Accrual Enhanced Yield through Strategic Credit Exposure

This hybrid note combines a Range Accrual with credit-spread capture, offering higher yields by referencing sovereign or corporate credit.

-Capital Protection: 100% (Provided no Credit Event occurs).

-Corridor Range: [0.0% – 4.8%/0.0% – 5.75%/0.00% – 5.75%] on the 10Y UST.

-Issuer Call: Quarterly after Year 1.

-Coupon: Paid out Quarterl

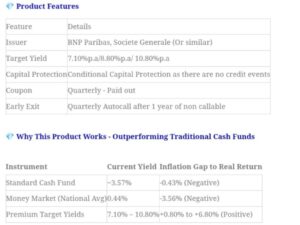

Featured Issuer: Emirate of Abu Dhabi

5 Year: 7.10% p.a.

7 Year: 8.80% p.a.

10 Year: 10.80% p.a.

Other reference entities available on demand include Airbus, UBS, Societe Generale, BNP Paribas, Volkswagen, and various Sovereign states.

While traditional cash funds are currently yielding approximately 3.5% to 3.7% (e.g., Vanguard Treasury Money Market at 3.62%), these structured products are specifically engineered to outperform standard liquidity tools:

1-Yield Superiority: With target coupons ranging from 4.80% to 10.80%, these notes provide a clear margin over the current 3.57% SOFR and average money market yield.

2-Institutional Grade Issuers: These products are issued by major global financial institutions such as BNP Paribas and Societe Generale, ensuring high-tier credit quality.

3-Secondary Market Liquidity: While designed to be held to maturity or call, a secondary market exists, providing a path for liquidity if circumstances change.

4-Preserving Real Terms: At 4% inflation, traditional cash funds barely break even in real terms. These structures are designed to provide a positive real return even as energy costs filter through the supply chain.

Next Steps – Let’s organise a technical briefing call

This structured product is designed for those looking to secure return in an environment of uncertainty.

If you are reviewing liquidity mandates for the remainder of 2026, I am available for a technical briefing to review underlying issuers and the specific mechanics of participation. Please do not hesitate to write me a message or request a call.

Note: This communication is provided for informational purposes only as a single product concept and does not constitute financial, investment, or legal advice.

Rebecca Jane Ellis Consultancy (ARIF Swiss Client Advisor)| rebecca@rebeccajaneellis.com

X-@theGBJournal|Facebook-the Government and Business Journal|email:gbj@govbusinessjournal.com|govandbusinessj@gmail.com

{kind=link}